Sunday, May 03, 2020

Sunday, April 12, 2020

The Use and Abuse of MMT

The Use and Abuse of MMT

By Michael

Hudson, with Dirk Bezemer, Steve Keen and T. Sabri Öncü

Michael

Hudson is a research professor of Economics at University of Missouri, Kansas

City, and a research associate at the Levy Economics Institute of Bard College.

His latest book is “and forgive them their debts”:

Lending, Foreclosure and Redemption from Bronze Age Finance to the Jubilee Year

Dirk

Bezemer is a Professor of Economics at the University of Groningen in The

Netherlands

Steve

Keen is a Professor and Distinguished Research Fellow at the Institute

for Strategy, Resilience and Security of University College London (www.isrs.org.uk). He blogs at https://www.patreon.com/ProfSteveKeen

T.

Sabri Öncü (sabri.oncu@gmail.com) is an economist based in İstanbul, Turkey

Summary

After being attacked by monetarists and others for many decades, MMT

and the idea that running government budget deficit is stabilizing instead of

destabilizing is suddenly gaining applause from the parts of the political

spectrum that long opposed MMT: the banking and financial sector, especially

the Republicans. But what is applauded is in many ways something quite different than the leading MMT advocates have long supported.

Modern Monetary Theory (MMT) was developed to explain the logic of

running government budget deficits to increase demand in the economy’s

consumption and capital investment sectors so as to maintain full employment.

But the enormous U.S. federal budget deficits from the Obama bank bailout after

the 2008 crash through the Trump tax cuts and Coronavirus financial bailout

have not pumped money into the economy to finance new direct investment,

employment, rising wages and living standards. Instead, government money

creation and Quantitative Easing has been directed to the finance, insurance

and real estate (FIRE) sectors. The result is a travesty of MMT, not its original

aim.

By subsidizing the financial sector and its debt overhead, this

policy is deflationary instead of supporting the “real” economy. The effect has

been to empower the banking sector, whose product is credit and debt creation

that has taken an unproductive and indeed extractive form.

This can clearly be seen by dividing the private sector into two

parts: The “real” economy of production and consumption is wrapped in a

financial web of debt and rent extraction – real estate rent, monopoly rent and

financial debt creation. Recognizing this breakdown is essential to distinguish

between positive government deficit spending that helps maintain employment and

rising living standards, as compared to “captured” government spending to

subsidize the FIRE sector’s extraction and debt deflation leading to chronic

austerity.

Origins and policy aims of MMT

MMT was developed

to explain the monetary logic in running budget deficits to support aggregate

demand. This logic was popularized in the 1930s by Keynes, base on his idea of

a circular flow between employers and wage-earners. Deficit spending was seen

as providing public employment and hence consumer spending to absorb enough

production to enable the economy to keep producing at a profit. The policy goal

was to maintain (or recover) reasonably full employment.

But production and

consumption are not the entire economy. Modern Monetary Theory (MMT) was formally

developed in the 1990s, with roots that can be traced by Abba Lerner’s theory

of functional finance, and by Hyman Minsky and others seeking to integrate the

financial sector into the overall economic system in a more realistic and

functional way than the Chicago School’s monetarist approach on the right wing

of the political spectrum. A key point in its revival was Warren Mosler’s

insight that a currency-issuing country does not “tax to spend”, but instead

must spend before its citizens can pay tax in that currency.

MMT was also Post-Keynesian

in the sense of advocating government budget deficits as a means of pumping

purchasing power into the economy to achieve full-employment. Elaboration of

this approach showed how such deficits created stability instead of the

instability that results from private-sector debt dynamics. At an extreme, this

approach held that recessions could be cured simply by deficit spending. Yet

despite the enormous deficit spending by the U.S. and Eurozone in the wake of

the 2008 crash, the overall economy continued to stagnate; only the financial

and real estate markets boomed.

At issue was the

role of government in the economy. The major opponents of public enterprise and

infrastructure, of budget deficits and market regulation, was the financial

sector. “Austrian” and Chicago-style monetary theorists strongly opposed MMT, asserting

that government budget deficits would be inflationary, citing Germany’s Weimar

inflation of the 1920s, and Zimbabwe, and portraying government deficits (and

indeed, active government programs and regulation) as “interference” with “free

markets.”

MMTers pointed out

that running a budget surplus, or even a balanced budget, absorbed income from

the economy, thereby shrinking demand for goods and services and leading to

unemployment. Without government deficits, the economy would be obliged to rely

on private-sector banks for the credit needed to grow.

That occurred in

the United States in the final years of the Clinton administration when it

actually ran a budget surplus. But with a public sector surplus, there had to

be a corresponding and indeed identical private sector deficit. So the effect

of that policy was to leave either private debt financing or a trade surplus as

the only ways in which economic growth could obtain the monetary support that

was needed. This built in structural claims for interest and amortization that

were deflationary, ultimately leading to the political imposition of debt

deflation and economic austerity after the 2008 debt crisis.

Republican and financial sector opposition to budget

deficits and MMT

If governments do

not provide enough purchasing power by running budget deficits to enable the

economy to grow, the role of providing money and credit will have to be relinquished

to banks – at interest, and for purposes that the banks decide on (mainly,

loans to buy real estate, stocks and bonds). In this respect banks are

competitors with government over who will provide the economy’s money and

credit – and for what purposes.

Banks want the

government out of the way – not only regarding money creation, but also for financial

and price policies, tax policy and laws governing corporate behavior. Finance

wants to appropriate public monopolies, by taking payment in natural resources

or basic public infrastructure when governments are, by policy rather than

necessity, short of their own money, or of foreign exchange. (In times past,

this required warfare; today foreign debt is the main lever.)

To get into this

position, banks need to block governments from creating their own money. The

result is a conflict between private bank credit and public money creation.

Public money is created for social purposes, primarily to maintain production

and consumption growth. But bank credit nowadays is created largely to finance

the transfer of property and financial assets – real estate, stocks and bonds.

Opposing the logic for running budget deficits

The Reagan-Bush

administration (1981-82) ran budget deficits not to pay for social spending,

but as a result of tax cuts, above all for real estate.[1] The resulting budget deficit led to proposed

“cures” in the form of fiscal cutbacks in social spending, starting with Social

Security, Medicare and education. This aim became explicit by the Clinton

Administration (1993-2000), and President Obama convened the Simpson-Bowles

“National Commission on Budget Responsibility and Reform” in 2010. Its name

reflects its recommendation that “responsibility” meant a balanced budget,

which in turn required that social spending programs be rolled back.

Opponents of

public spending programs saw the rise in government debt resulting from budget

deficits as providing a political leverage to enact fiscal cutbacks in spending. Many Republicans and “centrist” Democrats had

long sought a reason to scale back Social Security. Austrian and Chicago-School

monetarists urged that government shrink its activity, privatizing as many of

its functions as possible to let “the market” allocate resources – a largely

debt-financed market whose resource and monetary allocation would shift away

from governments to financial centers – from Washington to Wall Street, and in

other countries to the City of London, the Paris Bourse and Frankfurt. However,

no such critique was levied against military spending, and the government

responded to the 2000 dot.com and 2008 junk-mortgage financial crises by

enormous monetary subsidy and bailouts of the economy’s credit and asset

sector.

The Obama and Trump financial bailouts as a travesty

of MMT

To advocates of

MMT, and indeed to most post-Keynesian economists, the positive function of

budget deficits is to spend money and therefore income into the economy. And by

“the economy” is meant the production-and-consumption sector, not the financial

and property markets. That “real” economy could have been saved in a number of

ways. One way would have been to scale back mortgage debts (and debt service)

to realistic market prices and rent rates. Another would have been simply to

create monetary grants and subsidies to enable debtors to remain in their

homes. That would have kept the financial system solvent as well as employment

and existing home ownership rates.

But Obama

double-crossed his voters by not rolling out bad mortgage debts and other

obligations to realistic market prices, and instead bailing out the banks for

credit creation in the form of bad loans (“liars’ loans” to NINJA borrowers),

and bad financial bets on derivatives by brokerage firms that were designated

as “banks” in order to receive Federal Reserve credit and bailouts. With bank

balance sheets impairing their ability to create new credit, the government

stepped in by creating its own credit. This gave the banks, shadow banks and

other non-bank financial institutions a bonanza of credit – replete with the opportunity

to buy up foreclosed homes and create rental properties. This policy was

organized by Blackstone, and turned the crisis into an opportunity to make

enormous rates of return for its participants. The effect was to intensify the

economy’s polarization, as investors typically needed a minimum $5 million

tranche to join.

The Federal

Reserve’s $4.6 trillion in Quantitative Easing did not show up as money

creation, because it was technically a swap of assets – like Aladdin’s “new

lamps for old, in this case “good credit for junk.” The effect of this swap was

much like a deposit inflow. It enabled banks to ride out the downturn while

making a killing in the stock and bond markets, and to lend for takeover loans

and related financial speculation.

Wall Street’s Financial capture of MMT to inflate

asset prices, not revive the economy

At issue is how to

measure “the economy.” For the wealthy One Percent, and even the Ten Percent,

“the economy” is “the market,” specifically the market value of the assets that

they own: their real estate, stocks and bonds. This property and financial

wrapping for the “real” production-and-consumption economy has steadily risen

in proportion to wages and industrial profits. It has risen largely by

government money and credit creation (and tax breaks for property and finance),

along with its economic rent, interest and financial charges and service fees,

which are counted as part of Gross Domestic Product [GDP], as if they were actual contributions to the “real” economy.

So we are dealing

with two economic spheres: the means of production, tangible capital and labor

on the one hand (what is supposed to be measured by GDP), and the market for financial

and property assets, along with their rentier

charges that are taken from the

income earned by this labor and real capital.

Financial

engineering replaces industrial engineering – along with political engineering

by lobbyists seeking tax breaks, rent-extraction privileges, and government

subsidy. To increase property and financial asset prices and corporate

behavior, companies are drawing on credit and government subsidy not to

increase their production and employment, but to bid up their stock prices by

share buyback programs and high dividend payouts. Buybacks are called “repaying

capital,” so literally this policy is one of disinvestment, not investment. It

is favored by tax laws (taxing “capital” gains at a lower rate or not at all,

as compared to taxes on dividends).

The blind spot of vulgarized MMT: The FIRE sector vs.

the “real” economy

Much superficial

confusion between the FIRE sector and the production-and-consumption economy

comes from repeating the over-simplification of classical monetary formula

MV=PT, namely, dividing the economy into private and government sectors. Setting

aside the balance of payments (the international sector), it follows that

government spending will pump money into the domestic economy, and that

conversely, budget surpluses will suck money out.

The problem is

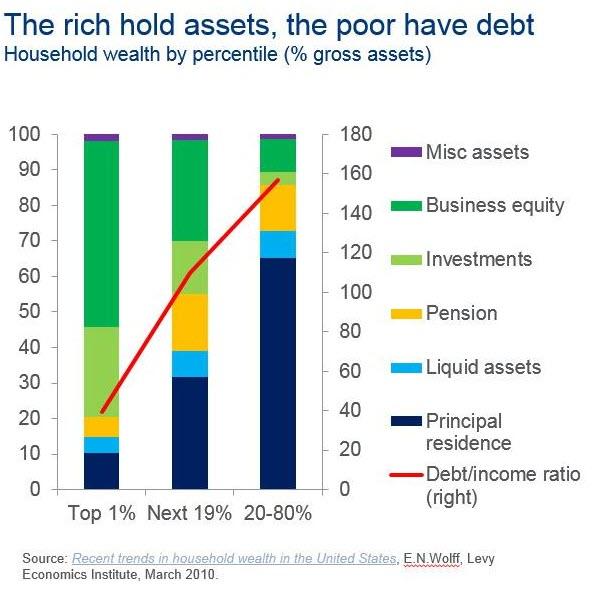

that this analysis, used by many MMTers, for instance, the Levy Institute’s

typical chart, does not distinguish between government spending into the FIRE

sector and asset markets as compared to spending into the “real” economy on

employment and production (including the building of public infrastructure, for

instance). Without this distinction it is not possible to see whether deficit

spending is productive by aiming at supporting employment and output, or merely

aims at supporting asset prices and making sure that creditors do not lose the

value of their financial claims on debtors – claims that have become unpayable

and thus are a bottomless pit of government deficit spending in the end.

Trying to keep the

financial sector and its debt overhead afloat implies imposing austerity on the

rest of the economy, IMF-style. So “MMT for Wall Street” is an oxymoron, and is

the opposite of MMT for a full employment economy.

MMT, public and private debt

Money is debt. Government

money creation for public purposes – to pay for employment and output – spurs

prosperity. But in its present form, private-sector debt creation has become

largely extractive, and thus leads to the opposite effect: debt deflation.

Governments can

pay public debt without defaulting, as long as this debt is denominated in

their own domestic currency, because the governments can always print the money

to pay. To the extent that public debt results from spending that supports

output, employment and growth, this process is not inflationary. The government

gives value to money by accepting it in payment of taxes. So the monetary

system is inherently bound up with fiscal policy. The classical premise of such

policy has been to minimize the economy’s cost structure by taxing mainly

unearned income (economic rents), not wages and profits in the

production-and-consumption sector.

The problem nowadays

is private debt. Most such debt is created by banks. This bank credit – debts

owed by bank customers – tends to increase faster than the ability of debtors

to earn enough income to pay it. The reason is that most of private debt is not

used for productive, income-generating purposes, but to finance the transfer

property ownership (affecting asset prices in proportion to the rate of credit

growth for such purposes). That use of credit – not associated with the

production-and-consumption economy – leads to debt deflation. Instead of

providing the economy with purchasing power (as in running government budget

deficits), private debt works over time to extract interest and amortization

from the economy, along with servicing fees.

The typical

mortgage, including its interest charges ends up exceeding the value that the

property seller received. As a result of compound interest, the mortgage debt

is repaid several times to the bank. The effect is to make banks the main

recipient of rental income (as mortgage debt service) and ultimately the main

beneficiaries of “capital” gains (that is, asset-price gains).

What gives bank

credit its monetary characteristics – and enables debt to be monetized as a

means of payment – is the government’s willingness to treat banks as a public

utility and guarantee bank deposits (up to a specified limit) and ultimately to

guarantee bank solvency.

A budget deficit resulting from a financial

bailout reflects the inability of the economy to carry its exponentially

growing debt overhead. Because this overhead increases as a result of the

mathematics of compound interest, the size of bailouts must increase – and with

it, the budget deficit (plus swap agreements) to subsidize this debt overgrowth

as an alternative to imposing losses by banks and financial investors.

That is what we

have seen since the financial crisis of 2008, both in Europe and the United

States. Led by the financial sector, much of the economic mainstream finally

has come to embrace the idea of budget deficits – now that these deficits are

benefiting primarily the financial and other parts of the FIRE sector, not the

population at large, that is, not the “real” economy that was the focus of

Keynesian economics and MMT.

This kind of

endorsement for government money creation thus should not be considered an

application of MMT, because its policy goal is almost diametrically opposite.

Much as the Reagan-era budget deficits were used as the first part of a one-two

punch to roll back social spending (Social Security, Medicare, education,

etc.), so today’s Obama-Trump deficits are being used to warn that the economy

must preserve fiscal “stability” by rolling back social programs in order to

bail out the financial economy. Wall Street magically has become transmogrified

into “the economy.” Labor and industry are viewed simply as deadweight

expenditures on the financial sector and its attempted symbiosis with the

central bank and Treasury.

The Financial Sector, Private Capital and Austerity

and Central Planning

If Wall Street is

bailed out once again at the expense of the “real” economy of production and

consumption, America will have turned decisively away from democracy into a

financial oligarchy. Ironically, the initial logic is the claim that an active

state is inherently less efficient than the private sector, and thus should be

shrunk (in the words of lobbyist Grover Norquist, “to a size so small that it

can be drowned in a bathtub”). But relinquishing resource allocation to the

financial sector leads to its product – that is, debt – creating a crisis that

requires unprecedented government intervention to “restore order,” defined as

saving banks and financial investors from loss. This can only be achieved by shifting

the loss onto the economy at large.

Today, the

financial sector – banks and financial investors – play the role that the

landlord did in the 19th century. Its land rents made Britain and

continental Europe high-cost economies, as prices exceeded cost-value. That is

what classical economics was all about – to bring market prices in lines with

actual, socially and economically necessary costs of production. Economic rent

was defined as unnecessary costs, which were merely payments for privilege: hereditary

landownership, and monopolies that creditors had carved out of the public

domain or won as legal compensation for financing public war debts.

The rentier class not only was the major

income recipient of the economic surplus, it controlled government, via the

upper house – the House of Lords in Britain, and similar houses across

continental Europe. Today, the Donor Class controls electoral politics in the United

States, via the Citizens United ruling. Political office has become privatized,

and sold to the highest bidders. And these are from the financial sector – from

Wall Street and financialized corporations.

The post-2008

stock market and bond-market boom raised the DJIA from 8500 to 30,000. This

gain was engineered by central bank support far in excess of what a “free

market” would have priced stock at. Before QE, U.S. shares had fallen only

slightly below the market average for the previous century. QE drove it to its

highest level outside the 1929 and 2000 bubbles. Even after the Coronacrash,

shares are still overpriced compared to pre-“Greenspan Put” prices.

The result is best

thought of as a blister, not a bubble. Its only hope of surviving without

bursting is for the government to continue to support it in the face of a

drastically shrinking post-coronavirus economy.

So the question is

what will be saved: The economy’s means of livelihood, or an oligarchy of

predators living in luxury off this shrinking livelihood?

All this was

explained by classical economists in their labor theory of value, which was

designed to isolate economic rent and other non-production overhead charges

(perceived to be mainly services in the 18th and 19th

century, especially by the wealthy classes).

The Hudson Paradox: Money, Prices and the Rentier

Economy

Without

distinguishing between the FIRE sector and the “real” economy there is no way

to explain the effects of government budget deficits on asset-price inflation

and commodity-price inflation.

Here is a seeming

paradox. Bank credit is created mainly against collateral being bought on

credit – primarily real estate, stocks and bonds. The effect of increasing

loans against these assets is to raise their prices – mainly for housing, and

secondarily for financial securities. Higher housing costs require new home

buyers to take on more and more debt in order to buy a home. Their higher debt

service leaves less disposable income to spend on goods and services.[2]

The asset-price

inflation effect of money creation by banks is thus to exert a downward impact on commodity prices, to

the extent that the carrying cost on bank credit reduces the net purchasing

power of debtors to buy goods and services. This deflationary effect of bank

money ends in a bad-debt crash, to which the government responds by bailing out

the financial sector with a combination of money creation and central bank

swaps (which do not appear as money creation). This is just the reverse of the

MV = PT tautology, which only measures the volume

of new money (M) without considering its use

– what it is spent on. By failing to distinguish the use of bank credit to buy

assets (hence, adding to asset-price inflation) as compared to government

deficit spending, both the old monetary formulae and the frequent MMT contrast

between public and private sectors neglect the need to distinguish the FIRE

sector’s “wealth and debt” transactions from how wages and profits are spent in

the production-and-consumption economy. The commercial banking system’s

“endogenous” money creation takes the form of credit at interest. The volume of

this interest-bearing debt grows exponentially, absorbing and extracting more

and more income from industry and labor. The effect on the overall economy is

debt deflation

It may be

epitomized as

Give a man a fish, and you feed him for a day;

Teach him how to fish, and you lose a customer.

But give him a loan to buy a boat and net to fish, and he will end

up paying you all the fishes he catches. You have a debt servant.

[1] Real estate was

given a fictitiously short accelerated depreciation allowance – as if a

building lost its entire value in just 7½ years, providing all rental income to

be charged as an expense and even to generate a fictitious tax-accounting tax

loss. This catalyzed the great conversion of rental properties to co-ops.

Landlords (called “developers”) took out a mortgage equal to the entire market

price of the building, and then sold apartments at a price not only greater

than zero, but typically equal to the entire mortgage. It was one of the great

“wealth creation” ploys in modern history. And it was left out of the National

Income and Product Accounts (NIPA), which used “realistic” depreciation – which

still pretended that buildings were losing value, despite the maintenance and

repair expenditures to prevent such loss.

[2] Higher stock and bond prices lower the

yield of dividend income. (Most such income is spent on new financial assets,

not goods and services, so the effect of lower yields probably is minimal, and

may be offset by a “wealth effect” of higher asset prices and net worth.)

Tuesday, April 07, 2020

How can the UNCTAD $2.5 trillion coronavirus aid package to developing countries be financed at no cost to anyone?

The current SDR basket is as follows:

Recently, 1 U.S. Dollar has been around 0.73 SDR so let me fix this exchange rate for simplicity. With this assumption, the proposed UNCTAD coronovirus aid package would be 1.825 trillion SDR. Although there currently are 19 countries in the eurozone, since what I propose costs nothing to any country, I pick the largest eurozone economy, namely, Germany, to represent the eurozone in my description of the mechanism also for simplicity. It is up to the eurozone countries to decide how exactly to contribute their shares to the package, assuming that they agree with what I propose.

Note from the above table that 1.825 trillion SDR is the sum of below amounts in the component currencies:

What I propose is that the treasuries of the United States, Germany, China, Japan and the United Kingdom inject capital to the IMF by issuing zero-coupon perpetual bonds in their own currencies in the above respective amounts. I call these bonds the corona bonds. Since the IMF can maintain deposit accounts in the central banks of the above countries (in the case of Germany, in the European Central Bank), the IMF can sell the corona bonds to the central banks of the respective countries for increased balances in its deposit accounts for the respective amounts.

Hence, 1.825 trillion SDR is created for the IMF at no cost to these five countries and since the IMF deposits at these central banks are not reserves, there is no change in the base money of any of the countries.

{kind=link}

Tuesday, March 24, 2020

Thursday, March 19, 2020

I was interviewed on Imran Kahn's international appeal to foreign creditors

My answers are in black.

This week Pakistan's Prime Minister Imran Khan issued an international appeal asking the developed countries to wave off debt of struggling economies such as Pakistan. He says that the impact of the coronavirus will make things difficult for developing countries in coming months.

I've been asked to write a story, which briefly explains if this is even possible.

It is not only possible but also a must. There is no alternative. TINA!

Is there any precedent for something like this where the developed countries have deferred or waived off part of their debt to poor countries in wake of calamity?

History is full of examples. Just look at West Germany as one example. How do you think West Germany has become one of the wealthiest countries after what happened to her during World War II? At the time, Germany was one of the largest debtors to foreign creditors. Leaving aside massive cancellations (about 90%) of domestic debts as part of the German Currency Reform of 1948 which made West German citizens and corporation to start from an almost clean slate, the London debt agreement of 1953 relieved West Germany from 51% of her foreign debt.

The London debt agreement between West Germany and 20 external creditors wrote off 46% of her pre-war debt and 52% of its post-war debt. The remaining was converted into long-term low-interest loans with a five-year grace period before repayment. Furthermore, Germany had to repay its debt only if it ran a trade surplus, and all repayments were limited to 3% of annual export earnings. Then came the economic miracle of West Germany. Why can we not do something similar for poor countries under current conditons? We must.

What would happen if countries like Pakistan which are dependent on exports to EU and US see a slowdown? What if remittances from the middle east go down?

Isn't answer to these questions obvious? Horrible things would happen. Imran Kahn explained to the foreign creditors what would happen very nicely. What more can I say?

Do you think Khan has a strong case here?

He has a very strong case. All developing countries should line up behind him and ask for debt relief from their foreign creditors including official creditors such as the IMF and the World Bank. Not only their public debts to their foreign creditors, but also the foreign debts of their non-financial private sectors must be restructured and large parts of all these debts must be written-off. As Michael Hudson always says, debts that cannot be paid will not be, so we better cancel those that cannot be paid.

Sunday, February 16, 2020

Muhteşem bir video (İngilizce) - Princes of the Yen

Japonya'ya da Türkiye'ye olanlar oldu. Yani, bırakın Türkiye'yi, o tarihlerde Japonya'ya da aynı şeyi yaptılar. İbret için izleyin.

Friday, February 14, 2020

Bir bankayı banka olmayan kurumlardan ayıran nedir?

Yasalardır tabii ki. Banka olmayan kurumlar ikiye ayrılır. Finansal olmayan kurumlar (FOK) ve banka olmayan finansal kurumlar (BOFK). Bu ikisini bir araya getip bunlara BOK diyelim. Lütfen ama bunu dışkı anlamına almayın. Kısaltma yalnızca.

BOKlar da, bankalar da 100 lira kredi verdiklerinde bilançoları şöyle değişir ilk aşamada:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı + 100

——————————————————

Buraya kadar bir farklılık yok. Farklılık bir sonraki aşamada.

BOK:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı 0

Kasa - 100 l

——————————————————

Toplam 0 l Toplam 0

Bu arada, tediye ödeme demek. Yani BOKlar tediye hesaplarındaki yükümlülüğü kasalarından ödemek zorundalar. Dolayısıyla, kredi verdiklerinde bilançoları büyümez. Yalnızca varlıklarının kompozisyonu değişir

Ama bankalar bu yasaya tabii değiller. Onlarınki şöyle ikinci aşamada.

BANKA:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı 0

l Mevduat + 100

——————————————————

Toplam + 100 l Toplam + 100

Bunu nasıl yapabiliyorlar? Çünkü BOKların tabii oldukları yasalardan muhaflar ve tediye hesabının adını mevduata çeviriyorlar. Mevduat da paradır. Bankalar böyle para üretiyorlar ve kredi verdiklerinde bilançoları büyüyor. Bankaları da BOKlara uygulanan yasalara tabii kılın, bankalar da para üretemez hale gelirler, yalnızca finansal aracı olurlar ve ortalık karışır. O zaman parayı kim üretecek Hazine ve Merkez Bankası aralarında paslaşarak üretmezlerse?

BOKlar da, bankalar da 100 lira kredi verdiklerinde bilançoları şöyle değişir ilk aşamada:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı + 100

——————————————————

Buraya kadar bir farklılık yok. Farklılık bir sonraki aşamada.

BOK:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı 0

Kasa - 100 l

——————————————————

Toplam 0 l Toplam 0

Bu arada, tediye ödeme demek. Yani BOKlar tediye hesaplarındaki yükümlülüğü kasalarından ödemek zorundalar. Dolayısıyla, kredi verdiklerinde bilançoları büyümez. Yalnızca varlıklarının kompozisyonu değişir

Ama bankalar bu yasaya tabii değiller. Onlarınki şöyle ikinci aşamada.

BANKA:

VARLIKLAR l YÜKÜMLÜLÜKLER

____________________________________

Kredi + 100 l Tediye Hesabı 0

l Mevduat + 100

——————————————————

Toplam + 100 l Toplam + 100

Bunu nasıl yapabiliyorlar? Çünkü BOKların tabii oldukları yasalardan muhaflar ve tediye hesabının adını mevduata çeviriyorlar. Mevduat da paradır. Bankalar böyle para üretiyorlar ve kredi verdiklerinde bilançoları büyüyor. Bankaları da BOKlara uygulanan yasalara tabii kılın, bankalar da para üretemez hale gelirler, yalnızca finansal aracı olurlar ve ortalık karışır. O zaman parayı kim üretecek Hazine ve Merkez Bankası aralarında paslaşarak üretmezlerse?

Friday, February 07, 2020

Ben bakmazken dolar 6 lirayı geçmiş

Ne diyeyim? Hayırlısı olsun! Şunu da hatırlatayım. 2020'ye girdiğimizde, sanırım Ocak başı, lira konusunda artık bir şeyler olabilir demiştim. Önümzüdeki günlerde göreceğiz neler olacağını.

Thursday, February 06, 2020

ABD'de Demokrat Parti Çalkalanıyor Ama

Hiç önemi yok. Demokrat Parti'den başkan adayı kim çıkarsa çıksın, bu seçimi Trump kazanacak. Bütün gelen sinyaller ona işaret ediyor. Zor günler bu günler. Faşistler kazanıyor. Demokrat Parti sol filan değil ama sol çaresiz. Alternatif sunamıyor. Bernie bile sunamıyor. İngiltere'de Corbyn de sunamadı ve gitmek zorunda kaldı. Bir başka sıkıntı daha. Bernie de Corbyn de çok yaşlılar. Yaşlı olmaları değil de sorun, solun başını çekebilecek gençler çıkmıyor. Sıkıntı orada. Yoksa Bernie ve Corbyn'in yaşlı olmalarında değil. Sol, liderlik sıkıntısı çekiyor her yerde. Türkiye'de de.

Monday, February 03, 2020

Seminer: "Para nedir? Parayı kim üretir?" - 22 Şubat 2020, 14:00-18:00, Beşiktaş, İstanbul

4ware Akademi seminerlerinden ilkine katılmak isteyenler sabri.oncu@gmail.com adresime yazarak kayıt olabilirler.

Saturday, February 01, 2020

Keynes'in tanımıyla ABD, 2000 Üçüncü Çeyrekten beri depresyonda.

Keynes depresyonu şöyle tanımlıyor: "önemli bir süre boyunca iyileşme veya çökme yönünde belirgin bir eğilimi olmadan kronik bir normal-altı aktivite durumu." Bu tanımın tek sıkıntısı normali nasıl tanımlayacağın ama çok zor da değil. En basit tanımı dönem öncesinin ortalamasıdır ki elimizdeki veriler 1948 Birinci Çeyrek'ten başlıyor. NASDAQ 2000 Nisan'ında göçtü. Dolayısıyla, 2000 öncesinin ortalamasına bir bakalım ve 2000 sonrasının resmini çizelim:

O kesikli yatay çizgi 1948 Birinci Çeyrek - 1999 Dördüncü Çeyrek arasındaki ortalama reel büyüme. Resimden görüldüğü gibi, ABD ekonomisi reel büyümesi 2000 Üçüncü Çeyrek itibarıyla ortalamanın altına iniyor ve 78 çeyreklik bir süre içerisinde ne bir iyileşme ne de bir çökme eğilimi gösteriyor. Ek olarak 2000 Üçüncü Çeyrek - 2019 Dördüncü Çeyrek arası ortalama reel büyüme %2, 1948 Birinci Çeyrek-1999 Dördüncü Çeyrek arası ortalama reel büyüme %3.6.

O kesikli yatay çizgi 1948 Birinci Çeyrek - 1999 Dördüncü Çeyrek arasındaki ortalama reel büyüme. Resimden görüldüğü gibi, ABD ekonomisi reel büyümesi 2000 Üçüncü Çeyrek itibarıyla ortalamanın altına iniyor ve 78 çeyreklik bir süre içerisinde ne bir iyileşme ne de bir çökme eğilimi gösteriyor. Ek olarak 2000 Üçüncü Çeyrek - 2019 Dördüncü Çeyrek arası ortalama reel büyüme %2, 1948 Birinci Çeyrek-1999 Dördüncü Çeyrek arası ortalama reel büyüme %3.6.

Dolayısıyla, Keynes'in tanımıyla 2000 Üçüncü Çeyrek'ten beri depresyonda ABD.

Dolayısıyla, Keynes'in tanımıyla 2000 Üçüncü Çeyrek'ten beri depresyonda ABD.

ABD 30 Yıllık (30Y) Hazine Faizi %2 altında

30Y faizi tarihinde ilk kez %2 altına 2019 yazında düşmüştü. Dün yine düşmüş. Pek olan bir şey değildir. 10Y faizi de %1.5 altına gitti gidecek. Bu zaten olacaktı da nCoV-2019 süreci hızlandırdı.

Friday, January 31, 2020

Dünya Sağlık Örgütü mü, Dünya Ticaret Örgütü mü?

Dün Dünya Sağlık Örğütü’nün nCoV-2019 açıklamasını şaşkınlıklar içerisinde dinledik: durum acil ama siz yine de devam edin filan gibi bir şey. Yani, halk sağlığının ne önemi var, mühim olan paradır, uluslararası ticaret ve seyahat sürsün. Dünya Ticaret Örgütü böyle bir şey deseydi şaşırmazdık da, diyen Dünya Sağlık Örgütü olunca, ben biraz şaşırdım tabii.

Wednesday, January 29, 2020

nCoV-2019 giderek kötüleşiyor

Bırakın dünyanın gerisini, nCoV-2019 yalnızca Çin’in ekonomisini vursa ki kötü vuracağı açık, dünya ekonomisi sarsılır. Her gün hastalığın baştan düşünüldüğünden daha bulaşıcı ve öldürücü olduğu görülüyor. Altın (ve diğer değerli metaller) ve güvenli ülke tahvilleri dışında kalan finansal varlık ve emtia piyasaları da sarsılacaktır. Köpükler patlayacaklar.

Paranın Miktar Teorisi neden yanlıştır?

Werner şurada anlatıyor.

Özetlemek için önce terimleri tanımlayalım.

M: Para miktarı

V: Paranın dolaşım hızı

P: Mal ve hizmetlerin ortalama fiyat seviyesi

T: Ortalama fiyattan alınan mal ve hizmet miktarı

GSYİH: Gayrı Safi Yurt İçi Hasıla (Yurt İçi Gelir)

Paranın Miktar Teorisi şunu diyor.

M: Para miktarı

V: Paranın dolaşım hızı

P: Mal ve hizmetlerin ortalama fiyat seviyesi

T: Ortalama fiyattan alınan mal ve hizmet miktarı

GSYİH: Gayrı Safi Yurt İçi Hasıla (Yurt İçi Gelir)

Paranın Miktar Teorisi şunu diyor.

MV = PT = GSYİH

Bunun yanlış olmasının nedeni de bütün paranın (yani

M'in) yalnızca üretilen mal ve hizmetlere yapılan harcamalarda kullanılmıyor

olması. Ve tabii burada maldan kasıt üretilen mal. Tarlaya mal demiyoruz. Gerçi

tarla alımı da tarlayı satana gelir olarak yazılıyor (ne diye milli muhasebe

hesapları yanlıştır diyorum?) ama üretilen bir şey yok bu alış-verişte.

Dolayısıyla, paraların hepsini bir torbaya

koymaktansa, iki ayrı torbaya koymak gerekir: 1) Üretilen mal ve hizmetlere

harcanan para (Mg olsun) 2) Var olan varlıklara harcanan para (Ms

olsun. Yani:

ve burada:

M = Mg + Ms

ve burada:

Mg: Üretilen mal ve hizmetlere harcanan para (GSYİH arttıran para)

Ms: Var olan varlıklara harcanan para (GSYİH arttırmayan para)

Mesela, mahalledeki kahveden aldığınız çaya harcadığınız para Mg torbasında, Boğaz'da yalı almak için harcadığınız para Ms torbasında ve tabii bu iki torba arasında gidiş gelişler de oluyor. Yani bu değişkenler statik değiller. Dinamik değişkenler. Ama şimdilik orayı karıştırmayalım.

Bu torbalara karşılık gelen diğer değişkenler de şunlar olsun: Vg, Pg, Tg ve Vs, Ps, Ts.

Dolayısıyla elimizde 2 ilişki var:

İlki:

Mg*Vg = Pg*Tg = GSYİH (harcamalar üretimden çok tüketime yapılırsa bildiğiniz enflasyon olur)

İkincisi:

Ms*Vs = Ps*Ts = RİBA yoluyla KENZ (buradan varlık fiyatı enflasyonu olur)

2000'den bu yana yapılan parasal genişlemeler çokluk Mg değil Ms torbasına gittiklerinden o parasal genişlemeler pek işe yaramadılar. Gelir ve servet dağılımındaki eşitsizliğin nedeni de bu: Ms artarken (riba yoluyla kenz), Mg pek artmıyor, hatta para Mg torbasından çıkıp Ms torbasına gidiyor.

Özetlersek, paranın miktar teorisi bu nedenle (yani bütün parayı tek torbaya koyduğundan) yanlıştır.

Tuesday, January 28, 2020

Monday, January 27, 2020

ABD 10 Yıllık Hazine faizi %1.6'ya düşmüş

Daha da düşecek. %1 altına bile düşebilir. Engelleyip engelleyemeyeceklerini birlikte göreceğiz. Unutmayın ama. Ben bu nCoV-2019'dan çok önce ABD faizleri düşecek diyordum, çoğunluk yükselecek derken.

Hala öyle diyorum.

Hala öyle diyorum.

22 Şubat'ta "Para Nedir, Parayı Kim Üretir?" Toplantısı - İstanbul - Beşiktaş

İlgilenenler sabri.oncu@gmail.com adresime yazabilirler. 14:00-18:00 arası olacak. Sohbet olacak, bir bilenin bilmeyenlere zorlayacağı bir şey değil. Her tür itiraz kabülüm. Yeter ki gün eksilmesin penceremden. Konunun önemi de şurada: bu konu anlaşılmadan, dünya ekonomik ve finansal sistemi anlaşılamaz.

Para Nedir, Parayı Kim Üretir?

Toplantının amacı katılımcısını 1694'te kurulmuş olan İngiliz Merkez Bankası (Bank of England) ile başlamış olan Modern Bankacılık Sisteminin işleyişiyle tanıştırmaktır. Doğaldır ki hiçbir sistem başladığı gibi sürmez. Sürekli evrilir. Dolayısıyla, 1694 öncesi ve sonrasında olanların tarihinden hareketle anlatılacak olan bugündür. Bu anlatımda, 19. yüzyıldan bu yana çeşitli dönemlerde baskın olmuş üç bankacılık teorisi ve kıyılarda kalmış bir dördüncüsü tartışılacaktır. Bu bankacılık teorileri, kıyıda kalmış dördüncüsü bir yana, tarihsel baskınlık sırasıyla şunlardır: 1) Kredi Yaratma Teorisi, 2) Kısmi Rezerv Teorisi, 3) Aracılık Teorisi ve 4) Paranın Devlet Teorisi. Bugünlerde (özellikle ABD Başkanlık Seçimi nedeniyle) ABD'de meşhur olmuş Modern Para Teorisi (MMT) bu teorilerin dördüncüsünün bugüne uzantısıdır. Bankacılık sistemi bilançoları üzerinden bu teoriler karşılaştırılıp, doğru olanın hangisi olduğuna birlikte karar verilecektir.

Dr. T. Sabri Öncü

ABD finans piyasalarında uzun yıllar çalışmış bir finansal iktisatcı olan Öncü, eğitimini Boğaziçi, Alberta, California-Berkeley ve Stanford Üniversitelerinden aldı. Drezdner-RCM Küresel Yatırım (Drezdner-RCM Global Investors) Şirketinde Sabit Gelir Araştırma Bölümü Direktörlüğü, Hindistan Merkez Bankası (RBI) İleri Finansal Araştırma ve Öğrenim Merkezi (CAFRAL) Baş İktisatcılığı, Birleşmiş Milletler Ticaret ve Gelişme Konferansı (UNCTAD) Kıdemli İktisatcılığı gibi görevler yapmış olan Öncü, Boğaziçi, Alberta, New York, Donau, Bilkent, Kadir Has ve Sabancı Üniversitelerinde matematik, finans ve iktisatın çeşitli dallarında lisans, lisansüstü (MBA) ve doktora düzeylerinde dersler verdi. Saygın uluslararası dergilerde akademik ve günlük gazete, dergi ve elektronik yayınlarda güncel çok sayıda makale yayımlamış olan Öncü, halen Hindistan dergisi the Economic and Political Weekly, H. T. Parekh Finans Sütunu yazarıdır.

Para Nedir, Parayı Kim Üretir?

Toplantının amacı katılımcısını 1694'te kurulmuş olan İngiliz Merkez Bankası (Bank of England) ile başlamış olan Modern Bankacılık Sisteminin işleyişiyle tanıştırmaktır. Doğaldır ki hiçbir sistem başladığı gibi sürmez. Sürekli evrilir. Dolayısıyla, 1694 öncesi ve sonrasında olanların tarihinden hareketle anlatılacak olan bugündür. Bu anlatımda, 19. yüzyıldan bu yana çeşitli dönemlerde baskın olmuş üç bankacılık teorisi ve kıyılarda kalmış bir dördüncüsü tartışılacaktır. Bu bankacılık teorileri, kıyıda kalmış dördüncüsü bir yana, tarihsel baskınlık sırasıyla şunlardır: 1) Kredi Yaratma Teorisi, 2) Kısmi Rezerv Teorisi, 3) Aracılık Teorisi ve 4) Paranın Devlet Teorisi. Bugünlerde (özellikle ABD Başkanlık Seçimi nedeniyle) ABD'de meşhur olmuş Modern Para Teorisi (MMT) bu teorilerin dördüncüsünün bugüne uzantısıdır. Bankacılık sistemi bilançoları üzerinden bu teoriler karşılaştırılıp, doğru olanın hangisi olduğuna birlikte karar verilecektir.

Dr. T. Sabri Öncü

ABD finans piyasalarında uzun yıllar çalışmış bir finansal iktisatcı olan Öncü, eğitimini Boğaziçi, Alberta, California-Berkeley ve Stanford Üniversitelerinden aldı. Drezdner-RCM Küresel Yatırım (Drezdner-RCM Global Investors) Şirketinde Sabit Gelir Araştırma Bölümü Direktörlüğü, Hindistan Merkez Bankası (RBI) İleri Finansal Araştırma ve Öğrenim Merkezi (CAFRAL) Baş İktisatcılığı, Birleşmiş Milletler Ticaret ve Gelişme Konferansı (UNCTAD) Kıdemli İktisatcılığı gibi görevler yapmış olan Öncü, Boğaziçi, Alberta, New York, Donau, Bilkent, Kadir Has ve Sabancı Üniversitelerinde matematik, finans ve iktisatın çeşitli dallarında lisans, lisansüstü (MBA) ve doktora düzeylerinde dersler verdi. Saygın uluslararası dergilerde akademik ve günlük gazete, dergi ve elektronik yayınlarda güncel çok sayıda makale yayımlamış olan Öncü, halen Hindistan dergisi the Economic and Political Weekly, H. T. Parekh Finans Sütunu yazarıdır.

Genç bir arkadaş böyle bir kitap yazmış

Hocam, eleştirilerini katkı görürüm diye bana göndermiş. Hoşuma gidiyor böyle şeyler. Daha çok böyle kitaplar yazılsın. Ama daha da önemlisi, bunlar okunsun.

Bir ders de bu konuda vereceğim: Davos 2020 sonrasında dünya

Ergin Yıldızoğlu

Milyarderler de durumun farkındalar ama çözüm tahayyül edemiyorlar.

Borçlar Silinsin, Ücretler Arttırılsın, Varsıllardan Varlık Vergisi Toplansın!

Bunlar da tek başlarına çözüm değiller ama yine de çözüme giden yolda atılması gerekli adımlar.

Milyarderler de durumun farkındalar ama çözüm tahayyül edemiyorlar.

Borçlar Silinsin, Ücretler Arttırılsın, Varsıllardan Varlık Vergisi Toplansın!

Bunlar da tek başlarına çözüm değiller ama yine de çözüme giden yolda atılması gerekli adımlar.

Sunday, January 26, 2020

Servet vergisi konusunda dediklerim çok radikal geliyorsa, buyrun bu çocuğu dinleyin - İngilizce

Geçen yıl Davos’ta demiş. Milyarderler bu yıl davet etmemişler. Çok zenginlerden %90 servet vergisi alınsın diyor. Ben de öyle demiyor muyum? 1 milyarlık serveti olana 900 milyon vergi. 100 milyon kime yetmez?

Doğruyu söyleyen dokuz köyden kovulur diyorlar ya. Bu çocuğa da öyle olmuş.

Vuhan Coronavirus üzerine söylentiler virusten hızlı yayılıyor.

Söylentilerin doğru olup olmadıkları önemli değil. Psikolojik etkileri önemli. Çin’in tek viroloji enstitüsünün Çin Bilimler Akademisine bağlı Vuhan Viroloji Enstitüsü olması söylentilerin kaynağı. Vuhan Coronavirus için Çin’in Çernobili diyenler var. Bakalım bu olay nereye gidecek?

Saturday, January 25, 2020

Coronavirus ırkçılığı arttırıyor.

Çinliler yarasa, köpek, yılan yiyiyorlar ve bu hastalık yarasa ve yılanlarda başlamış ya. Ondan. Çinli düşmanlığı artıyor. Bu da Çin’in yükselişine zarar verecek. Yani sırf bir sağlık sorunu değil bu hastalık. Politik, ekonomik ve finansal etkileri de var. Bu kadar sıkıntılı bir zamanda ortaya çıkabilirdi.

Friday, January 24, 2020

Coronavirus sonunda hisse senetlerini vurdu

Hızla dünyaya yayılıyor. Piyasalar ayılmakta geç bile kaldılar. Gerçi gerçek ekonomik sorunlar karşısında yeni coronavirus hiçbir şey ama neyse.

Bu benim derse benziyor ama biraz daha teknik

https://cef.sabanciuniv.edu/sertifika-programlari/finansin-temelleri-yatirimlar/

Dört gün olunca daha teknikleşmek mümkün. Benimki 8 saatlik olacak ve türevler olmayacak. Tabii ben fazladan neden bunların yanlış ve zararlı olduklarını anlatacağım. Halbuki burada onlar doğrudur diye anlatılıyordur muhakkak. Gerçi sabit gelir fiyatlamasında sorun pek yok. Orada diğer finansal varlıkların fiyatlamasından çok daha başarılıyız. Bunlar standart MBA konuları ve hala bunları doğrudur diye anlatıyorlar MBA programlarında. Yanlış oldukları bilindiği halde. Ne diyebilirim?

Dört gün olunca daha teknikleşmek mümkün. Benimki 8 saatlik olacak ve türevler olmayacak. Tabii ben fazladan neden bunların yanlış ve zararlı olduklarını anlatacağım. Halbuki burada onlar doğrudur diye anlatılıyordur muhakkak. Gerçi sabit gelir fiyatlamasında sorun pek yok. Orada diğer finansal varlıkların fiyatlamasından çok daha başarılıyız. Bunlar standart MBA konuları ve hala bunları doğrudur diye anlatıyorlar MBA programlarında. Yanlış oldukları bilindiği halde. Ne diyebilirim?

Çin’de 10 şehir karantinada

Bu virüs çok ters zamanda ortaya çıktı. Yayılmayı sürdürürse piyasaları kötü etkiler. ABD faizlerindeki düşüş, tahvil piyasasının benimle hemfikir olduğunu gösteriyor. Şikago’da da görülmüş. Paniğe neden olursa, ortalık kötü karışır. Zaten karışacak da, hemen karışır.

İlk ders konusunda gelişme.

17 Mart 2020, Salı günü birgünlük olacak. Dersi bir kurum üzerinden vereceğim için ücret ve yer bilgileri henüz elime geçmedi. Geçince bildiririm. Bunları kurum belirliyor. Ben yalnızca gidip dersi vereceğim. Başka yerlerle de konuşuyorum. Gelişmeleri buradan duyururum. Bu arada, kurumun adı PKF Akademi.

Wednesday, January 22, 2020

Bu da ikinci dersin içeriği.

Para Nedir? Parayı Kim Yaratır?

Dersin amacı

katılımcısını 1694'te kurulmuş olan İngiliz Merkez Bankası (Bank of England)

ile başlamış olan Modern Bankacılık Sisteminin işleyişiyle tanıştırmaktır.

Doğaldır ki hiçbir sistem başladığı gibi sürmez. Sürekli evrilir. Dolayısıyla, 1694

öncesi ve sonrasında olanların tarihinden hareketle anlatılacak olan bugündür. Bu

anlatımda, 19. yüzyıldan bu yana çeşitli dönemlerde baskın olmuş üç bankacılık

teorisi ve kıyılarda kalmış bir dördüncüsü tartışılacaktır. Bu bankacılık teorileri

sırasıyla şunlardır: 1) Kredi Yaratma Teorisi; 2) Kısmi Rezerv Teorisi; 3) Aracılık

Teorisi ve 4) Paranın Devlet Teorisi. Bugünlerde (özellikle ABD Başkanlık

Seçimi nedeniyle) ABD'de çok meşhur olmuş Modern Para Teorisi (MMT) bu

teorilerin dördüncüsünün bugüne uzantısıdır. Bankacılık sistemi bilançoları

üzerinden bu teoriler karşılaştırılıp, doğru olanın hangisi olduğuna birlikte

karar verilecektir.

İkinci dersin başlığı: Para nedir? Parayı kim yaratır?

Bunun içeriğini henüz yazamadım ama bir kaç saate yazarım.

Nasıl başlık?

Nasıl başlık?

İlginç bir durum.

Bugün ayın 22'si ve bugün itibarıyla bu ay 8000 kişiyi geçmişim. Böyle bir şey daha önce olmadıydı. Ne oldu acaba? Böyle giderse, bu ay 10 bini geçecek gibi duruyorum. Bence iyi bir şey. Bana herhangi bir maddi katkısı olduğundan değil de manevi katkısı var. Bu denli aykırı olunca, buna rağmen izleyenlerin olduğunu görmek güç veriyor.

Böyle bir ders vereceğim. İlgilenen olur mu?

Finansal Okuryazarlık

Dersin amacı

katılımcısını temel finans piyasalarının analizine giriş için bilinmesi gerekli temel

finans ürünleri olan borç ve hisse ürünleri ve piyasalarıyla tanıştırmaktır. Dersin

kapsamı içerisinde tartışılacak araçlar, getiriler, verimler, faizlerin vade

yapısı, Markowitz Portföy Teorisi, Sermaye Varlık Fiyatlama Teorisi, borç ve

senet ürünlerinin fiyatlanması, bu temel ürünlerden oluşan portföylerin analizi

ve risklerinin yönetimi olacaktır. Ancak, bu araçların teknik ayrıntıları

değil, ne şekilde kullanıldıkları sorunlarıyla birlikte tartışılacaktır.

Parayla olacak tabii ve bir günlük bir program. İlgilenenler bana yazsınlar: sabri.oncu@gmail.com

Teknik olmayacak. Teknik olsa, bir günde bunlar anlatılamaz. Stanford finans PhD programında finansal iktisat dersinde anlatılıyor teknik halleri ve üç-dört ay sürüyor bunları anlatması, teknik anlatılırlarsa.

Söylemesi ayıptır, Stanford'ta o dersten H aldım. En yüksek nottur. Herkes alamaz ama o tarihte ben zaten o dersi verebilecek kadar konuyu biliyordum. Ama bu yüksek not alma garantisi değildir. Bir zamanlar dersini verebilecek kadar iyi bildiğim bir başka konu olan Sürekli Ortamlar Mekaniği dersinden, aldığım en kötü notlardan birini aldım. Hoca o kadar kötüydü ki, hadi lan, diye dersle ilgilenmeyi bıraktım ve sınavlarına çalışmadım. Ama Stanford'ta Finansal İktisat dersini veren çocuk çok iyiydi. Zevkle gittim derslerine. Yeni bir şey öğrendiğimi söyleyemem ama çocuğu seyretmesi çok hoştu. Bilenin bildiği gözüküyor.

Söylemesi ayıptır, Stanford'ta o dersten H aldım. En yüksek nottur. Herkes alamaz ama o tarihte ben zaten o dersi verebilecek kadar konuyu biliyordum. Ama bu yüksek not alma garantisi değildir. Bir zamanlar dersini verebilecek kadar iyi bildiğim bir başka konu olan Sürekli Ortamlar Mekaniği dersinden, aldığım en kötü notlardan birini aldım. Hoca o kadar kötüydü ki, hadi lan, diye dersle ilgilenmeyi bıraktım ve sınavlarına çalışmadım. Ama Stanford'ta Finansal İktisat dersini veren çocuk çok iyiydi. Zevkle gittim derslerine. Yeni bir şey öğrendiğimi söyleyemem ama çocuğu seyretmesi çok hoştu. Bilenin bildiği gözüküyor.

Monday, January 20, 2020

Ülkemizdeki finans terimlerini hiç sevmiyorum, kötü tercümeler olduklarından

İlk sevmediğim terim faiz. Allah'a ihanet baştan. Allah faiz mi diyor? Hayır. Riba diyor.

İkinci sevmediğim terim getiri. Tahvillerin verimine getiri diyorlar. Hayır. Getiri başka şey, verim başka şey.

Kiraya rant diyorlar. Sanki kira ranttan başka bir şeymiş gibi.

Fed'i FED yazanları da bir arkadaşın dediği gibi, vallahi sopayla kovalarım.

Arkadaşlar,

FED değil Fed;

Getiri değil verim (tahvil konusunda);

Rant değil kira;

Faiz değil riba;

Ki zaten riba kiradır!

İkinci sevmediğim terim getiri. Tahvillerin verimine getiri diyorlar. Hayır. Getiri başka şey, verim başka şey.

Kiraya rant diyorlar. Sanki kira ranttan başka bir şeymiş gibi.

Fed'i FED yazanları da bir arkadaşın dediği gibi, vallahi sopayla kovalarım.

Arkadaşlar,

FED değil Fed;

Getiri değil verim (tahvil konusunda);

Rant değil kira;

Faiz değil riba;

Ki zaten riba kiradır!

Marks'a düşman bir aklın sefaleti

Ergin Yıldızoğlu'nun yazısı

Marksist olmamak bir şey, Marks'a düşman olmak başka bir şey. Ben Marksist değilim mesela. Gerçek heterodoks benim gibi olur. Hani demiştim ya, ben imanlı ateistim. Gerçek heterodoksluk da öyle bir şeydir. Ama gerçek heterodoks Marks'a düşman olmaz. Olamaz. Her teoriden işe yarar bir şeyler çıkar ve bütün teorilerde sorunlar vardır ama benim gördüğümce bugünkü anaakım iktisatçıların teorileri yanında Marks'ın teorisi en akla yatanı. Keynes'inkine bile beş basar. Ve üstelik, Marks'ın teorisi komünizm üzerine değildir. Kapitalizm üzerinedir. Düşman olanlar, bunu bile bilmiyorlar.

Ergin şöyle bitiriyor:

"Karşımızda, tam anlamıyla, yeniden yüzdürülmesi olanaksız bir ekonomik, siyasi, ekolojik, entelektüel enkaz var. Parçalarından yeni bir şeyler yapabilmek için zaman hızla azalıyor."

Ve, maalesef, haklı.

Marksist olmamak bir şey, Marks'a düşman olmak başka bir şey. Ben Marksist değilim mesela. Gerçek heterodoks benim gibi olur. Hani demiştim ya, ben imanlı ateistim. Gerçek heterodoksluk da öyle bir şeydir. Ama gerçek heterodoks Marks'a düşman olmaz. Olamaz. Her teoriden işe yarar bir şeyler çıkar ve bütün teorilerde sorunlar vardır ama benim gördüğümce bugünkü anaakım iktisatçıların teorileri yanında Marks'ın teorisi en akla yatanı. Keynes'inkine bile beş basar. Ve üstelik, Marks'ın teorisi komünizm üzerine değildir. Kapitalizm üzerinedir. Düşman olanlar, bunu bile bilmiyorlar.

Ergin şöyle bitiriyor:

"Karşımızda, tam anlamıyla, yeniden yüzdürülmesi olanaksız bir ekonomik, siyasi, ekolojik, entelektüel enkaz var. Parçalarından yeni bir şeyler yapabilmek için zaman hızla azalıyor."

Ve, maalesef, haklı.

New York Times, Elizabeth Warren'ı destekliyor.

New York Times

İyi yapıyor. Warren, Sanders kadar radikal değil ama Biden'den iyidir. Servet vergisi bayrağını Sanders'den önce Warren açtı, ekonomistler Saez ve Zucman desteğiyle. O çocuklar da çok radikal değiller ama olsun. Servet vergisi radikal sayılır bugünlerde ve gerekli. Zaten mecburen gelecek. Türkiye'de AKP servet vergisine başladı bile.

İyi yapıyor. Warren, Sanders kadar radikal değil ama Biden'den iyidir. Servet vergisi bayrağını Sanders'den önce Warren açtı, ekonomistler Saez ve Zucman desteğiyle. O çocuklar da çok radikal değiller ama olsun. Servet vergisi radikal sayılır bugünlerde ve gerekli. Zaten mecburen gelecek. Türkiye'de AKP servet vergisine başladı bile.

Yine Sven Henrich: Gelir ve Servet Eşitsizliği Üzerine

Sven Henrich

Böyle diyor da hastalığı yanlış tanımlıyor. Bu gelir ve servet eşitliğinin nedeni Fed ve diğer büyük merkez bankalarının piyasaya bastıkları paralar nedeniyle şişen varlık fiyatları değil. Başka deyişle, Fed ve diğer büyük merkez bankalarının yaptıkları neden değil, sonuç. Gerçi bir geri besleme de olduğundan bir süre sonra nedensellik iki yönlü olmaya başlıyor ama olay çok daha karmaşık.

Buradan kansız nasıl çıkılabileceğini ben hayalleyemiyorum. Çok kan akacak. Varlık vergileri de gelmeli. Hem de çok büyük varlık vergileri. 3 ABD'linin serveti, ABD nüfusunun %50'sinin servetinden daha büyükse, buradan mecburen kan çıkar.

Görüyor musunuz varlıkların nasıl dağıldığını?

Böyle bir dünyada kandan başka bir şey çıkamaz.

QE mi, değil mi?

Financial Times makalesi

Ne olduğu hiç önemli değil. Birgün Fed'in bunu da durdurmak zorunda kalacağı önemli. O gün, çok acıklı birgün olacak.

Çok sevindim: Merkez’den Hazine’ye 55 milyar TL transfer bekleniyor

Devletin Para Yaratması - Türkiye Versiyonu

Biz yıllardır anlatıyorduk da millet anlamıyordu. Arkadaşlar, devlet de para yaratabilir. Nasıl yaratabileceğinin gözünüzün önünde bir örneği bu işte. Geçen yıl da yapılmıştı zaten. Geçen yıl yapıldığında ekonomi pek de öyle sarsılmadı bildiğiniz gibi. Ne diyorlardı anaakım arkadaşlar? Eyvah, batıyoruz diyorlardı. Gerçi battığımız doğru da, nedeni bu değil.

Biz yıllardır anlatıyorduk da millet anlamıyordu. Arkadaşlar, devlet de para yaratabilir. Nasıl yaratabileceğinin gözünüzün önünde bir örneği bu işte. Geçen yıl da yapılmıştı zaten. Geçen yıl yapıldığında ekonomi pek de öyle sarsılmadı bildiğiniz gibi. Ne diyorlardı anaakım arkadaşlar? Eyvah, batıyoruz diyorlardı. Gerçi battığımız doğru da, nedeni bu değil.

Çok şaşırdım: IMF Küresel Büyüme tahminini düşürmüş

Haberi

İyi yapmış. Yalan söylemenin de sınırları var. Birleşmiş Milletlerin tahmini çok daha düşük.

Kime inanacağız?

İyi yapmış. Yalan söylemenin de sınırları var. Birleşmiş Milletlerin tahmini çok daha düşük.

Kime inanacağız?

Sayın Albayrak Türkiye'nin negatif faizle ilk kez tanışmadığını, önemli olanın mominal faiz olduğunu kaydetti.

Haberi

İlginç bir iddia. Ama benim işime geliyor bu iddia. Ben hep ne diyorum? Kuran'da sözü geçen faiz reel faiz değil nominal (yani cari) faizdir diyorum. Önemli olan nominal faiz yani. Allah, nominal faizlerin sıfırlanmasını emrediyor. Allah'ın emrine uyulsun. Memleketteki bütün nominal faizler sıfırlansın. Sıfırlamayan, Allah'ın emrine uymayandır.

İlginç bir iddia. Ama benim işime geliyor bu iddia. Ben hep ne diyorum? Kuran'da sözü geçen faiz reel faiz değil nominal (yani cari) faizdir diyorum. Önemli olan nominal faiz yani. Allah, nominal faizlerin sıfırlanmasını emrediyor. Allah'ın emrine uyulsun. Memleketteki bütün nominal faizler sıfırlansın. Sıfırlamayan, Allah'ın emrine uymayandır.

Hindistan'ın Hayalet Kasabaları: Ödenemeyecek borçlar ödenmeyecekler!

Hayalet Kasabalar

Çok tanıdık bir sorun. Hindistan'da da bunlar oldu, Çin'de de, Türkiye'de de, Şili'de de ve liste öyle gidiyor. İnşaat üzerinden büyüme sıkıntılı bir büyüme. Ve birgün böyle oluyor. Bunlar bir Türkiye'ye olmuyor yani. Marx + Veblen + Minsky, neden böyle olduğunu hemen anlıyorsunuz. Önceden kestirilemez şeyler değiller bunlar. Bunların böyle olacağı bilgisi bana Allah tarafından vahiy yoluyla mı indi de böyle olur diyordum? Dış sermaye girişlerine bağımlı, borç artışına dayanan, inşaat odaklı büyüme modeli sonunda krize neden olur. Basit yani olay. İşin kötüsü, hükümetimiz hala Kanal İstanbul diyerek borç attırıp, inşaat yapacak. Yapmaması gerekir. Yanlış büyüme yolu.

Özgür'ün kitabından bir tablo:

Buradaki en büyük proje ne? İstanbul Havalimanı. Bu nedenle durdurulamadı. Kanal İstanbul da bu nedenle durdurulamayacak. O, İstanbul Havalimanı projesinden daha da büyük bir proje ve hükümetin büyüme modeli için gerekli. Ona karşı çıkılacaksa, borç üzerinden karşı çıkmak gerekir. Doğa, insanlar, haksızlık, rant üzerinden değil. Borç üzerinden.

Borç arttırarak inşaat üzerinden büyüme modelinden vaz geçilmesi talep edilmelidir. Karşı çıkanlar, yanlış yerden karşı çıkıyorlar.

Çok tanıdık bir sorun. Hindistan'da da bunlar oldu, Çin'de de, Türkiye'de de, Şili'de de ve liste öyle gidiyor. İnşaat üzerinden büyüme sıkıntılı bir büyüme. Ve birgün böyle oluyor. Bunlar bir Türkiye'ye olmuyor yani. Marx + Veblen + Minsky, neden böyle olduğunu hemen anlıyorsunuz. Önceden kestirilemez şeyler değiller bunlar. Bunların böyle olacağı bilgisi bana Allah tarafından vahiy yoluyla mı indi de böyle olur diyordum? Dış sermaye girişlerine bağımlı, borç artışına dayanan, inşaat odaklı büyüme modeli sonunda krize neden olur. Basit yani olay. İşin kötüsü, hükümetimiz hala Kanal İstanbul diyerek borç attırıp, inşaat yapacak. Yapmaması gerekir. Yanlış büyüme yolu.

Özgür'ün kitabından bir tablo:

Buradaki en büyük proje ne? İstanbul Havalimanı. Bu nedenle durdurulamadı. Kanal İstanbul da bu nedenle durdurulamayacak. O, İstanbul Havalimanı projesinden daha da büyük bir proje ve hükümetin büyüme modeli için gerekli. Ona karşı çıkılacaksa, borç üzerinden karşı çıkmak gerekir. Doğa, insanlar, haksızlık, rant üzerinden değil. Borç üzerinden.

Borç arttırarak inşaat üzerinden büyüme modelinden vaz geçilmesi talep edilmelidir. Karşı çıkanlar, yanlış yerden karşı çıkıyorlar.

Subscribe to:

Posts (Atom)